Required Compliance Documents

The Approvely team should collect the following documents before sending over to the Approvely Compliance team for initial review before submitting the merchant to the bank for bank approval. By clicking on the links below, you can see examples of each type of document.

Required Documents:

- Provide a clear overview of how each sweepstakes operates

- Withdrawal Limits

- Driver License of each Owner (25% or more ownership)

- geographical breakdown of where they operate

- Corporation Documents

- Compliance Additional Volume Forecasts

- BSA / AML Policy

- Flow of Funds Diagrams / Demo Videos

- Latest 3-6 Months Business Bank Statements

- If the merchant is net new, they must provide at least 1 or more of these supplementary docs. The more the better!

- Legal Opinon

- A legal opinion typically includes an attorney's written statement confirming compliance with specific laws or regulations, supported by evidence, analysis, and legal reasoning. This is typically several pages long (~80 pages more or less).

-

COC (Certification of Controls/3rd Party Audit

-

Proof of an automated KYC, Geolocation, Age Verification Provider

- Merchants will sometimes use the same provider for KYC, Geolocation, and age verification services. To show adequate proof they have automated KYC provider:

- Provide a signed contract showing the dates of service (must show ongoing service dates, not just one month's receipt)

- Service Level Agreement with provider outlining service provided include KYC, geolocation, and age verification

- Recording of your site demonstrating restricted access to the app/website from restricted territories / age groups

- Third-Party Certification or Audits confirming that their services are active and functioning correctly for the merchant's business

- Include examples of error/blocking screens for restricted locations or age groups

- Service Usage Analytics - Share monthly provider reports showing the number of KYC, geolocation, and age verifications. Include success/failure rates and data on blocked users.

- Merchants will sometimes use the same provider for KYC, Geolocation, and age verification services. To show adequate proof they have automated KYC provider:

-

Completion of merchant registration

- Merchants must register their accounts and confirm their merchant ID with the Approvely team upon completion

-

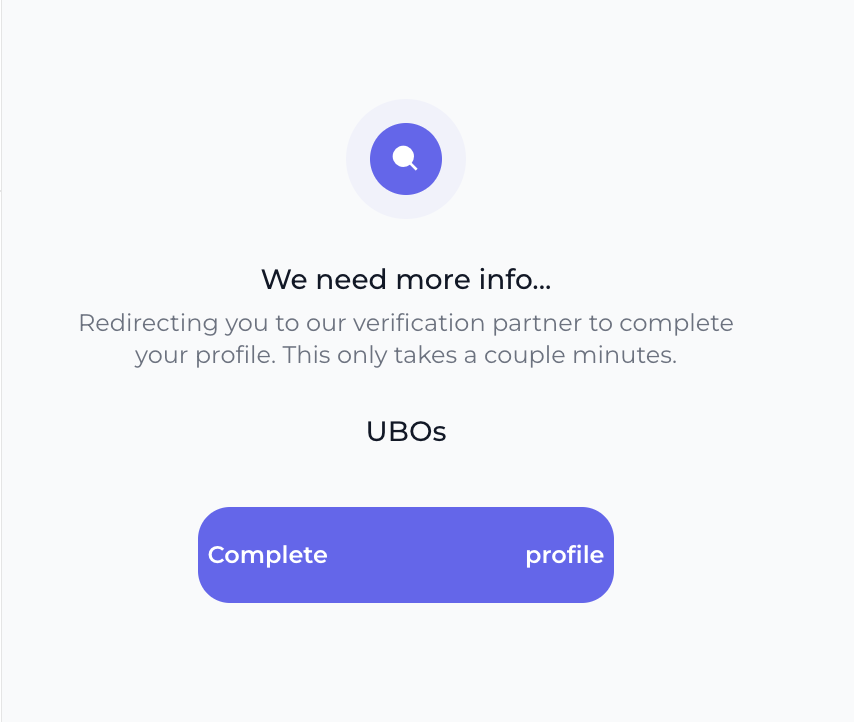

Completion of UBO verification on merchant dashboard

-

All UBOs (Ultimate Beneficiary Owners) must complete verification. The approvely team can confirm this by simulating the merchant account, and if the merchant sees a "We need more info..." prompt, direct the Merchant to have the specific UBO to login to the dashboard to complete verification from the homepage.

Example of what the Merchant sees when UBOs need to complete verification.

-

-

Signed Aptpay MSA

-

Signed Rapid MSA

-

Confirmation from Merchant they will utilize Chargeback protection (for card payments only)

- Merchants need to provide verbal agreement that they will leverage nSure/ chargeback protection services through the Rapid platform. This is something highly considered by the bank for approval.

-

Confirmation from Merchant they will utilize 3DS

- Merchants need to provide verbal agreement that they will leverage 3DS through the Rapid platform. This is required by the bank for approval.

- Provide a demo video showing how a customer is expected to register, login, play, make a payment, and withdraw.

Supplementary Documents:

Although not required for bank approval, please have the Merchant send the following documents. Adding additional documents will help build a stronger case to get the merchant approved, and can help get their acceptance rates higher.

- Historical Transaction Data

- Officer Certification

- Copy of Voided Check or Bank Letter

- Alternative documents that demonstrates the financial health and stability of the organization or key stakeholders